Originally published by Space Intel Report on February 20, 2025. Read the original article here.

Guillaume Faury. (Source: Airbus)

Guillaume Faury. (Source: Airbus)

LA PLATA, Maryland — Europe’s two biggest space-hardware builders, Airbus Defence and Space and Thales Alenia Space, have entered “preliminary, nonbinding” discussions on a merger of their satellite business, Airbus Chief Executive Guillaume Faury said Feb. 20.

The discussions include Leonardo of Italy, which owns one-third of Thales Alenia Space and two-thirds of satellite services provider Telespazio. Thales owns the remaining shares of both companies.

In a Feb. 20 investor call, Faury said the talks are limited to “satellites and satellite services,” which presumably would not include The Airbus and Thales Alenia Space exploration divisions, which build hardware for space stations and future lunar exploration.

Faury has been the most forward-leaning of the three companies’ chief executives in publicly citing the need for a large European company to be able to compete with SpaceX’s Starlink and the future Amazon Kuiper low-orbiting constellations.

“We expect to gain scale and speed by consolidating the business,” Fairy said. “We are in a business where scale matters, where technologies go very fast so you need to invest. To invest, you need scale to have a reasonable impact on the recurring costs, so you have to have scale in the production as well.

“We are in a situation where some U.S. players are disrupting the ecosystem, at scale, with new technologies in constellations. In Europe, at Airbus and also at Thales Alenia Space and Telespazio, we have technologies, in some cases even better ones. But we are missing the scale we need to be competitive in this new environment.

(Source: Airbus Feb. 20, 2025, investor presentation)

(Source: Airbus Feb. 20, 2025, investor presentation)

MBDA as a model

“So we want to scale. We want Airbus to have a stake in a large company. We would be happy if the end result looks something like the MBDA model, where we have a significant share with others in a business that can prosper, grow, invest and be successful on a global scale.”

Airbus owns 37.5% of missile-manufacturer MBDA, which is a joint venture with BAE Systems (37.5%) and Leonardo (25%).

Syndex, a European labor consultancy, in January concluded that the only consolidation that made sense was a full merger of the space divisions of Thales, Airbus and Leonardo.

Faury has previously said he would accept a partial merger, perhaps only of the satellite divisions, if that’s what it takes to win European regulatory and other government approval.

It remains unclear what effect the European Commission’s Iris2 multi-orbit secure communications constellation will have on negotiations among Airbus, Thales and Leonardo. The program is run as a 12-year concession managed by a consortium of European satellite fleet operators Eutelsat, SES and Hispasat.

It will not be known for several months what the precise work shares will be for the different Iris2 contractors, but Airbus would appear to be well-placed to build the 264 LEO-orbit satellites planned for the network given its most recent contract with Eutelsat for 100 OneWeb Gen 1 extension satellites, which will be compatible with Iris=2 but will not have all the Iris2 satellites’ features.

Even a limited merger including only the satellite divisions would have a major impact on employment in the city of Toulouse, France, where both Airbus and Thales Alenia Space have major manufacturing operations.

Faury acknowledged that even the contours of a merger had not been settled among the three companies.

“We are not at a point where we can fully answer the questions of what it will look like,” he said. “But what do we want? We want scale and speed in this business. We want to leverage the competencies and technologies we have, and for this we need to be up to the global competition, which is much more dollars and much more speed than ever.”

Airbus in 2023 began to take the measure of the difficulties in its Space Systems division by assessing the likely profitability of multiple contracts. The company’s OneSat software-defined satellite, which won a raft of early orders, has proven much more difficult than expected to produce. Other contracts, including the six Galileo positioning, navigation and timing satellites for the European Union, were won only after making a bid of dubious profitability.

Airbus has now revamped its bid/no-bid criteria.

“We are indeed selective in our orders,” Faury said. “In space… we took a lot of risks in development contracts, with a lot of new technologies, between 2018 and 2021.”

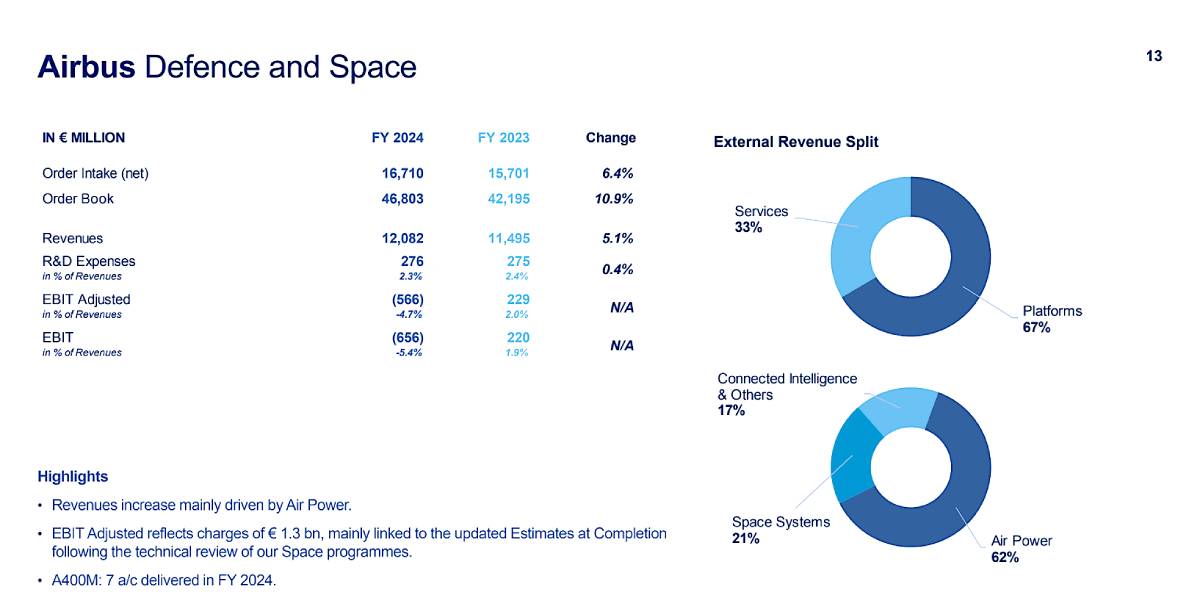

In 2023, the company booked a non-cash charge of 600 million euros (647 million) to account for a revision of the estimated cost at completion of certain satellite projects.

On Feb. 20, Airbus said the 2024 charges related to space system contracts totaled 1.3 billion euros, including 300 million euros on the fourth quarter.

Thomas Toepfer. (Source: Airbus)

Thomas Toepfer. (Source: Airbus)

Chief Financial Officer Thomas Toepfer said the fourth-quarter charge followed an in-depth technical review of the last major satellite program that had yet to be fully assessed, which resulted in “an update of key assumptions.”

“We had to go through the program bottom-up to fully review what we have in our portfolio. That we have done. We can now completely focus on what matters for the business, taking orders with good risk profile and focusing on orders and deliveries. The exercise of 2023-2024 is behind us,” Toepfer said. “This charge accounts for past, present and future profitability and hence only a portion of the charge relates to the current period.”

Airbus’s total adjusted pretax profit was 5.4 billion euros in 2024, down 6.9% from 2023, with the decrease attributed mainly to the satellite division charges.

“We are not expecting a negative cash burden on our space business in 2025,” Toepfer said. “The charges we took were mostly P&L related and only to a minor extent burdening our space business, so it has negative impact on profitability, as you can see, but we are not expecting any major cash charges in 2025.”

The Airbus Space Systems division reported 2.54 billion euros in revenue in 2024, up 10.3% from 2023.

Originally published by Space Intel Report on February 20, 2025. Read the original article here.