Orbith installation and service drivers logged 500,000 kilometers last year, the company says. It’s a key selling point. (Source: Orbith)

Orbith installation and service drivers logged 500,000 kilometers last year, the company says. It’s a key selling point. (Source: Orbith)

BUENOS AIRES — Satellite internet service provider Orbith SA of Argentina is one of several regional satellite service providers that are doubling down on their investments in the face of market incursion by SpaceX Starlink in addition to the global satellite fleet operators.

Orbith uses nine HTS beams — one from Hispasat’s Amazonas 3 and eight from SES’s SES-17 — and in 2023 signed an agreement with micro-GEO satellite builder Astranis. Orbith will now lease all the capacity on an Astranis GEO-orbit satellite to be launched over Argentina in 2025.

(Source: Space Intel Report photo by Amy Svitak)

(Source: Space Intel Report photo by Amy Svitak)

Orbith Chief Executive Pablo Mosiul said the Astranis satellite will be used alongside the existing capacity to bring Orbith’s customer base to 50,000 in 2026, compared to 20,000 now. In addition to Argentina, Orbith sells internet access in Chile, Paraguay and Uruguay.

In an interview at Orbith headquarters here, Mosiul outlined how a national satellite ISP, with so far little backing from the Argentine federal government, expects to maintain its market position at a time of increased competition.

Q: What is your current position in Argentina’s satellite internet market?

A: We are the biggest satellite operator in Argentina measured by the number of active VSATs. We had 10,000 connected in 2022 and will have 20,000 by the end of this year, with the goal of 50,000 in 2026. The second-largest player has 5,000 VSATs connected.

Orbith expects to reach 50,000 subscribers in 2026 after the launch of its Astranis satellite. (Source: Orbith)

Orbith expects to reach 50,000 subscribers in 2026 after the launch of its Astranis satellite. (Source: Orbith)

We are the biggest satellite operator in Argentina, by the amount of VSATs active. We will end this year with 20,000 active VSats for broadband access. The second player here has 5,000.

We are also the newest, we have been in the market for only seven years. We have grown very fast. We are the first to use HTS satellites here in Argentina. The first one was Amazonas 3, our first beam. We bought that capacity on Amazonas 3 in 2017 and then we bought eight additional beams from SES-17, in Ka-band.

And now we are building our first dedicated satellite.

What is the service offer today?

We offer up to 200 Mbps. The typical delivery is 100 Mbps but we can offer up to 200 Mbps. We also have tools that help us improve our efficiency, letting us determine who the subscriber is.

What is the breakdown between consumer/residential, government and enterprise customers?

We have three business segments. Sixty percent of our subscribers are residential users; 40% is deemed to be enterprise customers, some government services, for example, 2,000 rural schools connected to our network.

We also have a wholesale service that we offer to other telecommunications companies that sell the service under their own brand. This accounts for 30% of our business, so 70% is direct sales to users. We have both direct and wholesale business in our consumer and enterprise/government segments.

How is pricing evolving? Argentina is living through 100% annual inflation, which must make pricing difficult.

We have the lowest internet service price in the world — 100 Mbps for $40 per month. This is unique. No other company is offering 100 Mbps for $40 a month. There is no data cap, and it is a best-efforts service.

(Source: Orbith)

(Source: Orbith)

Can these prices hold off Starlink for the moment? Starlink in some markets has elected to reduce prices substantially to capture market share.

I think their prices will not be reduced much from the current point. In the U.S., Starlink is $110 a month. In Latin America it is half that price, $50 or $60 per month.

Given your Astranis micro-GEO agreement, you appear to believe that GEO can hold its own against LEO. Please explain your reasoning.

GEO is much more cost-efficient than LEO. LEO has a big advantage in terms of latency, no doubt about that. We understand that. But it’s much more expensive. The network is more complex, the terminal is much more complex and more expensive.

With GEO you can cover all of Argentina with one satellite. Starlink must launch 1,000 satellites per year just to maintain the network. It’s a matter of time for how long they can do that. Certainly Starlink can reduce the price but now, because of their launches.

Today we have a very competitive price. The one time payment with Starlink is about $500 for the terminal. But in this $500 you don’t have the installation keys, and so forth. You need that to install the service.

You can install it by yourself and the antenna works.

But if you have much wind, you may have a problem. You need installation support for the wall mount, cabling to go through the wall, a lot of things that you can buy but it adds up. It’s $100 for an apartment, and if you need more Wi-Fi access points, you pay $240 in additional costs.

So if you want to install the kit for all the devices in your house, you need to pay more than $1,000, just to connect your house, including the smartTV main console and your smartphone. You need more than is in the box, and you need someone to install the service on the roof.

Activate the series is not the same as installing the service. We include the installation in our cost, and our one time cost is $250, compared to with $500 to $1,000 or something in between.

So we have a very competitive price for installation. And we have a $40 monthly plan, where theirs is $60. And our offer is without data caps. It’s a competitive product that allows you to use Youtube and social networks, everything you need to work.

In Spain, there is a service from Hispasat and some ISPs for 35 euros per month, subsidized by the government, and Starlink is offering a service 29 euros per month.

We don’t have any government subsidies. We are profitable at these prices.

Your advertising stresses on-premises installation, after-sales service for maintenance and other advantages. How can you afford this?

We have 30 places where we have trucks and material and we deploy from those places to install and maintain. Some of them are employees and some are third-party providers that use our systems and our practices.

Starlink could offer this service as well.

Starlink does not have the staff. If at your house your SmartTV does not work with your access point, we send out a mission and solve the problem. Subscribers see the value of this and like it.

Who owns Orbith?

We have two founders and an investor, a board group that includes the owner of a family office that owns 70% of the company. The founders own 30% of the company.

Q: Are they long-term investors?

A: No, they are financial. We are on our third round and perhaps they will want an exit. They are (part of) a family office. Now we are working with some private equity funds.

(Source: Astranis)

(Source: Astranis)

How did you decide on the eight-year Astranis contract?

There was not enough satellite capacity in this region. It is not a question of demand, it’s capacity. When we started there was only one beam in Ka-band. We added SES 17 HTS because we needed a compeititve price with high bandwidth. We cannot use Ku.

Why can’t you use Ku-band?

The size of the antenna, the cost of the kit, and the capacity are higher. In Ka-band you have a cost-effective solution to meet our market segments. With Astranis, we will reduce the cost of our capacity by a lot.

At $10 million per year it’s still a lot less than leasing?

That is not what we are paying. I have an NDA with them and I cannot share that information. Somewhere this $80 million figure came up, but that’s not the number. The Astranis agreement allows us to reduce the cost of the capacity because with traditional satellite leases you have the manufacturer, the satellite operator and the service provider.

The satellite operator is trying to maintain margins that are no longer viable in this new context. They are discovering that, but it is taking time. If we don’t have satellite capacity we cannot succeed, so we leased a full satellite.

Astranis 8-year lease less costly than capacity lease on large-GEO satellite

To be clear: Leasing a GEO satellite’s full capacity for eight years is less expensive, per megabit delivered, than leasing capacity on a GEO?

From Hispasat, SES, Intelsat — any of them — yes. The economics are better in bigger satellites, in terms of cost per megabit, but then you need to fill that satellite in a given period of time. If not, the business plan will suffer. In our business plan we will fill the satellite in three years or less. Smaller satellites are better than leasing capacity from larger operators.

The cost per Mbps should be below $10 per month and it’s not possible to reach that value with SES or Intelsat. If you bet $300 million or $400 million for a satellite, you can reach that number. But this is too big for us. We would need 300,000 subscribers. We are talking about 50,000 to 100,000.

How does OneWeb fit into your plans?

We have an agreement with them and we will start offering LEO for corporate markets. LEO is expensive for commercial markets, and the latency is important. and a LEO-GEO combination is a good solution. We have lower cost in GEO and lower latency in LEO, and we can decide which network we use for which applications — streaming to GEO and other applications for LEO, for example. So we can provide a redundant service, and a low-latency service, at a lower price than what Starlink offers. They don’t have a multi-orbit offering.

Are you a OneWeb distribution partner?

A: Yes, we are now in the process of working with them. We are connecting with them at the PoP in Santiago. We have not started offering services yet but we will start soon.

Do you offer service-level agreement, an SLA?

Yes, we do.

Starlink doesn’t do that.

No, they don’t, and in some markets you need some specific requirements. Private networks, for example, can assign different priorities to different types of traffic. With OneWeb we can offer a high-value service to a private network.

Are there any other ISPs here that use OneWeb?

Most of them use Starlink and we think this is not a good idea. For example, Telespazio sells Starlink for corporate markets and Telefonica also is a seller of Starlink.

‘OneWeb is more friendly than Starlink’

But Starlink offers the service to them at the same price as Starlink offers to the end user. So if they want to charge more they have to add value, but the are competing against each other, so they have very little margin, and Starlink always wins.

OneWeb is more friendly. We are working with them and we can make good business from it. I like Starlink as a company. But I am trying to do business here.

Have you tried OneWeb here?

Yes. The latency is a little higher, from 70 to 100 milliseconds, so it’s not that low, but it’s lower than GEO. And the user experience is very good, despite the slightly higher latency.

You use high-resolution optical satellite imagery to pinpoint customer locations and then determine whether to offer service and, if so, how much to charge. Please explain this.

This is why we have the lowest price. We have people who analyze satellite pictures, to find out how many subscribers are in a given region. You can offer different service plans. And, depending on retention rate, we can offer a special plan. These are regions where fiber will never be available.

We will never sell in areas where the population is too dense. Churn is higher the more people you have per square kilometer. That makes sense. But older satellite companies like Hughes sell their service to anyone who wants to buy it. The churn is killing them. Hughes has a big problem with churn because they sold a lot in higher-population regions. Viasat did too.

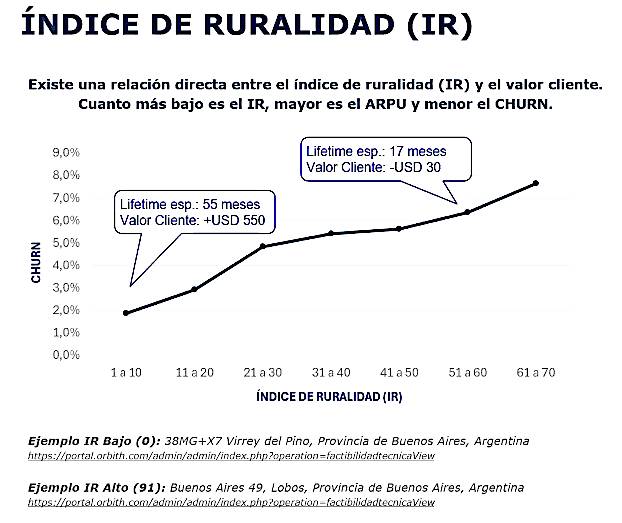

A customer that remains for 55 months is much more valuable than one that leaves after 17 months. Orbith’s index of rurality. (Source: Orbith)

A customer that remains for 55 months is much more valuable than one that leaves after 17 months. Orbith’s index of rurality. (Source: Orbith)

This is why their service is so expensive, Their customer retention is about 15 months. In our company, we get two years. We are using data analytics to determine metrics for each subscriber, including how difficult it is to reach a place. We can then tailor the offer. We could have an easy subscriber in terms of location, but it depends on how difficult it is to reach them and then the density of population. This helps us view our target markets and we only sell there. We are experts at selecting where our customers are.

Everyone wants internet. It’s easy to sell. The difficulty is to recognize where a high-value subscriber is, and where they are not.

Q: When you say churn will be higher, is that because fiber will be coming in?

A: Yes, because there are options in that area. Sometimes the customer buys the service because he had a problem with the previous service provider and its offer. Then the next month, they offer a discount, and they could move back to the previous operator. Wireless services are there, and fiber is growing.

(Source: Orbith)

(Source: Orbith)

A satellite offer will lose 60% of its customers in one year there. So we will not sell there. Sometimes training your sales people is not a solution. You must avoid having them sell in certain areas. Sales people always want to sell.

So now Orbith enters its expansion phase?

Yes. Last year we expanded our service to 100% of Argentina and Chile and we invested heavily in our service to start the next stage of our company.

Our installation and maintenance crews traveled 500,000 km last year — greater than the distance of the Earth from the Moon! — to service customers. Starlink doesn’t do that.

Why there is no government universal service program in Argentina?

There is one, but there are no programs for satellites. They use the money to invest in fiber.

What did the government think about your deal with Astranis? It got a lot of news coverage.

They like it. The government has a mission of supporting the private sector. They want open skies, so for them it’s good news.

Does the government not want to incentivize you, as a local operator, to battle the big guys?

They understand the situation. We have good relations with them. They know that competition works only if there are competitors. But for now they are not doing anything to protect us. We don’t have any kind of support from the government.

You have the 3,000 schools. Isn’t that a government contract?

Yes, but there is no subsidy there. They buy the service and pay for the service. And it/ss the provincial government that buys the eserine, We have agreements with several provinces, in four or five provinces.

Viasat and Hughes both have new, higher-capacity satellites over the Americas. Have you seen any effect on their competitive positioning in Latin America?

We are competing with Hughes in Chile, but Viasat is not there. They are not competing with us in Argentina. They had a problem with Viasat 3. Hughes has Jupiter 3 [a 500-Gbps satellite] and they are trying to sell service to us. They are not going to launch HughesNet service here. They do not appear to be growing in Latin America.

Did you ever think about being a service provider to Starlink?

We can use Starlink or Astranis and SES 17 and combine that into a multi-orbit service. Companies like Orbith have become multi-orbit providers.

Our contracts for the use of SES 17 and Hispasat’s Amazonas run to the satellites’ end of life. We need the new satellite to grow, not to remain where we are.

Who builds your antennas?

ST Engineering iDirect.

The Astranis satellite offers some payload flexibility in coverage, correct?

You cannot move the beams but you can move power and bandwidth from one beam to another, which is a flexibility we do not have with SES or Hispasat.