ALEXANDRIA, Va. — In the history of commercial satellite communication, no company has created more disruption than SpaceX’s Starlink. In just six years, Starlink has launched over 6,000 satellites and expanded its user base to 2.7 million subscribers—over one-third more than the combined 2 million subscribers of Hughes and Viasat at their peak. By the end of the year, Starlink will likely hit $6.6 billion in revenue, posting its first-ever cash flow positive year.

In ways, Starlink is only the beginning of an industry transformation. The evolution of Eutelsat OneWeb, the pending launch of Amazon’s Kuiper, Telesat’s Lightspeed and other LEO broadband constellations have left many traditional GEO operators wondering how they can compete.

Regional operators and service providers, in particular, are watching Starlink expand into new geographies and new market verticals. According to Novaspace analysis, Starlink accounted for approximately 85% of total usable high-throughput satellite capacity in 2023, including from GEOs. This has created a sense of crisis, where virtually every operator and service provider—regional and global—either has a Starlink strategy or they are actively developing one.

“They’ve really got three decisions: run, fight or partner,” said Brent Prokosh, a senior affiliate consultant at Novaspace, a merger of Euroconsult and SpaceTec Partners. “And we see they’re doing a mix of them.”

Home Field Advantage

Today, Starlink is the clear leader in consumer satellite broadband connectivity and it’s gaining ground in land mobility, aviation and the government sector. At least 75 countries currently allow Starlink, including a growing number in the Asia Pacific (APAC) region. Australia, the Philippines and Japan were among the early adopters in the region. More recently, Indonesia and Malaysia issued licenses allowing Starlink to operate within their borders.

Regional operators can attain market share and differentiate themselves against Starlink and other large LEOs, said Prokosh. “But it is tough to compete,” he noted. “It’s even more difficult to compete with Starlink regionally because of their small scale.”

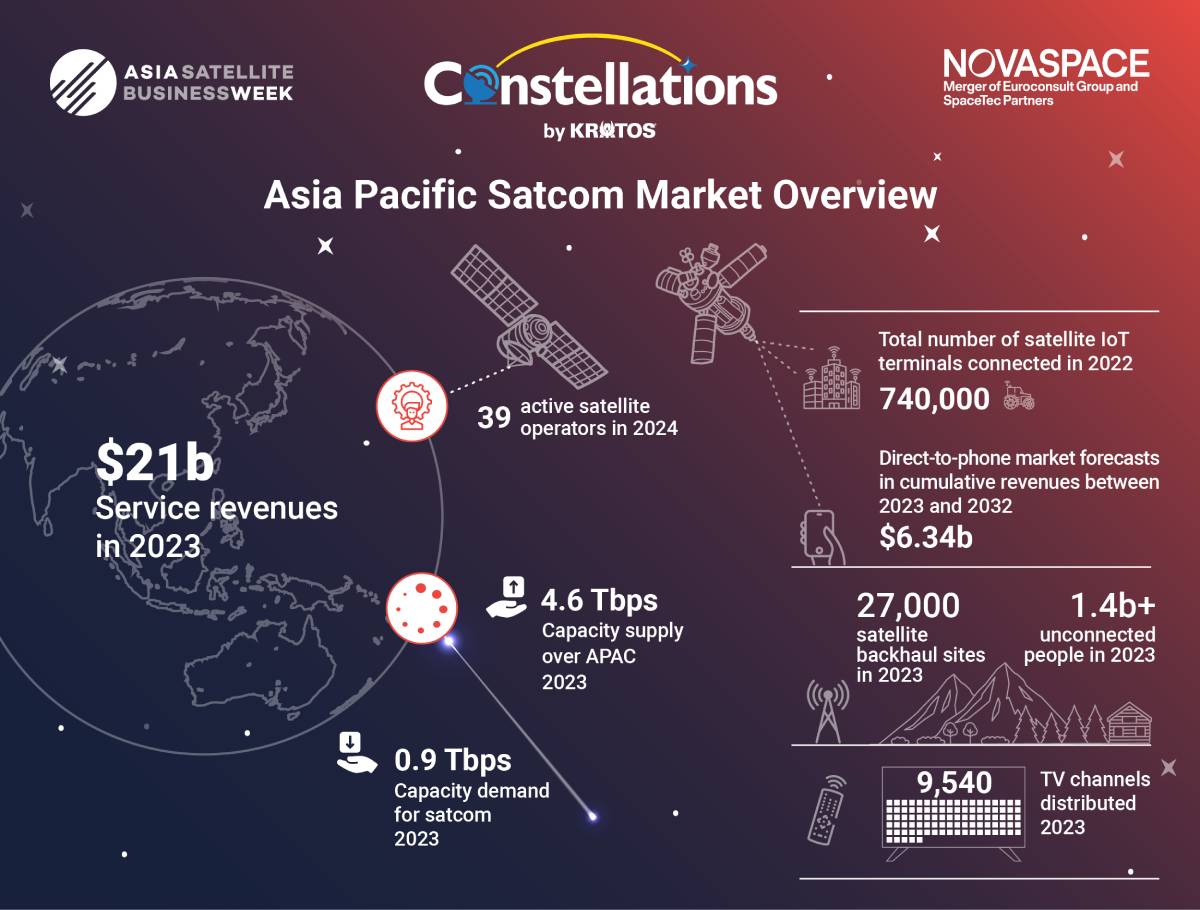

An overview of the APAC satellite communications market. (Source: Novaspace)

An overview of the APAC satellite communications market. (Source: Novaspace)

Still, there are areas where smaller, regional operators can and likely will continue to thrive against the LEO giants.

Sovereignty: While many countries in the Asia Pacific are opening their doors to Starlink, others are taking a more protectionist approach. Notably, India and China have refused to grant licenses to Starlink. The reasons may differ (e.g. building a robust national space economy, preventing access to global internet content, geopolitics) but all are ultimately underpinned by notions of sovereignty.

With some exceptions, defense and government customers are more inclined to award contracts to national or regional providers. Similarly, governments seeking to close the digital divide through Universal Service Obligation (USO) programs, such as Malaysia and Indonesia, are tending to look for local or regional providers or strong regional connections.

SLAs: For the satcom user that needs a service level agreement (SLA) with five nines availability, Starlink’s “best effort” service is probably not the most attractive option. Even though Starlink can provide speeds of 80 Mbps around 99% of the time, the uncertainty is particularly unsettling for defense customers as well as some mobility and enterprise customers.

In response to a question about how regional operators can compete with Starlink, ABS Chief Commercial Officer Ramsey Khanfour noted that his company’s “edge” is its agility, innovation and dedicated local support for customers. “We focus on mission critical and business grade applications where GEO solutions are well positioned,” he said.

There are also opportunities for GEO operators to field competitive services that have either higher data limits per month or guaranteed minimum speeds, according to business cases run by Novaspace. “This is definitely one of the opportunities there,” said Prokosh.

Looking into the future, Prokosh warned that operators “need to be careful about the general industry transition away from SLAs.” As usable satellite bandwidth becomes more abundant, some customers may opt for multiple low-cost, best-effort plans instead of a dedicated, higher cost SLA.

Broadcast: While satellite broadcast may be declining in North America and Europe, demand remains steady in Asia and other parts of the globe. GEOs and high throughput satellites (HTS) continue to dominate the video market, which still accounts for more than 80% of satellite services. That will continue to be the case over the next ten years, according to Novaspace projections, as video is still expected to generate at least half of satellite service revenue.

If You Can’t Beat ‘Em, Join ‘Em

It’s hard to beat the cost, value and performance mix Starlink brings to the satellite broadband market. Recent estimates by Quilty Analytics show Starlink unit economics at less than $50 per Mbps per month. The next generation v.2 minis, said to have four times the capacity of earlier generations, could lower those costs to less than $10 per Mbps per month based on saleable capacity.

For some industry players, the best answer to the Starlink question has been to buy or resell its service to supplement existing networks or offerings. For GEO providers, the addition of LEO services can be a major differentiator in terms of offering a multi-orbit, multi-network service. The redundancy of multiple orbits and networks avoids a single point of failure and brings flexibility to meet various customer requirements with a single, multi-service network.

Speedcast, a U.S.-based connectivity solutions provider and operator with a global footprint, welcomes the addition of new connectivity options—like Starlink, OneWeb or future Kuiper service—to its “connectivity toolkit.” Speedcast Executive Vice President of Global Sales and Marketing James Trevelyan explained that “a single, closed-network LEO service may not meet the mark in addressing and prioritizing [customer] requirements.” He continued, “So instead, these new options become part of the toolkit used to deliver a hybrid service for customers, in which an enterprise-grade SD-WAN technology converges multiple networks—from GEO, MEO and LEO satellite to fiber, microwave and cellular—into a single, high-performance WAN.”

While partnerships or “coopetition” can yield new value-added services, increase scale and reduce CAPEX, there are limitations. By moving away from the traditional wholesale lease model, operators stand to lose the margins many have become accustomed to, said Prokosh. “One of the cons of partnering with Starlink is they allow no markup of airtime or service costs on the connectivity layer,” he said. “Margins of 50%, 60% or more are not available in selling ancillary services off the back of Starlink.”

The path ahead for traditional global and regional players in the satellite industry will be challenging, especially as new LEO constellations start providing service over the next 1-3 years. But there are opportunities in forming partnerships, capitalizing on key differentiators and expanding services that can help traditional operators compete in a dynamic space.

Explore More:

Podcast with Kacific: Closing the Digital Divide in APAC

How the Satellite Industry Can Adapt to Starlink’s Aggressive Price Points

Is SD-WAN the Killer App for Multi-Orbit, Multi-Mission?

Dancing with a Colossus: Satellite Industry Fixated on Competition with SpaceX, Amazon