This file image shows Airbus workers in a cleanroom with the Galileo G2 satellite. (Source: Airbus)

This file image shows Airbus workers in a cleanroom with the Galileo G2 satellite. (Source: Airbus)

PARIS — The satellite manufacturing industry is witnessing a transformative phase driven by changes from end users and reflected in the satellite operators’ business model. As satellite-based services are moving toward more data-centric use cases, satellite manufacturers are poised to capture these new opportunities whilst still enjoying revenues from legacy businesses, like satellite broadcasting or government.

In a world where a handful of vertically integrated mega-constellations are concentrating and retaining in-house most of the demand, the manufacturing landscape is rapidly changing to secure its future. From software-defined payloads to cost-effective smaller GEO satellites and low-cost launch options, these new offerings are deemed to roll out tomorrow’s space segment.

Legacy GEO Comsat Demand Is Back but Most Contracts Won by New Vendors

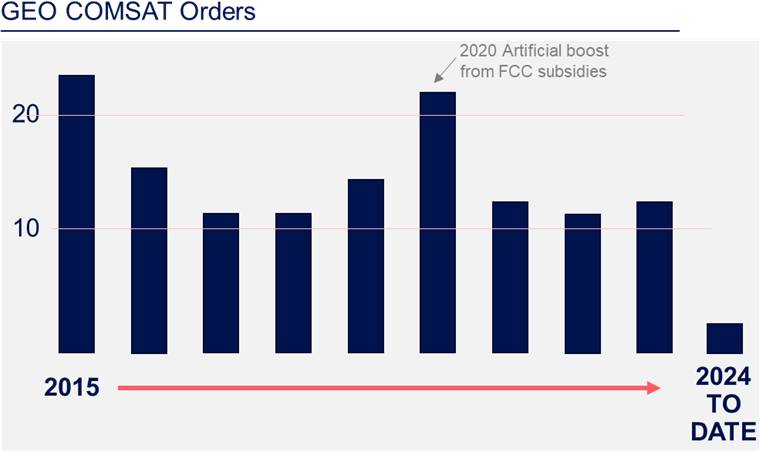

Beyond the hype about emerging commercial players, one shall repeat that legacy markets are still accounting for the lion’s share of this market jungle. After years of decline, Novaspace forecasts a moderate increase in GEO comsat demand, surpassing the levels of the past decade, with an average of 14 orders annually by 2032 compared to 12 in the past 10 years. This shift reflects the decline in broadcasting business and a transition toward the expanding broadband business, emphasizing the need for scalable solutions.

From Novaspace’s Satellites to be built and launched, 2024 (Source: Novaspace)

From Novaspace’s Satellites to be built and launched, 2024 (Source: Novaspace)

What Role for Smaller GEO?

Smaller GEO satellites are cheaper but have less capacity than their larger cousins. However, they are proving to be convincing for incremental capacity or new use cases. One-third of the 41 GEO orders placed since 2021 to date were won by new entrants through small GEO. Worth noting that satellite operators procured these smaller assets first and foremost to replace aging satellites that are reaching the end of their typical 15-year design lives, rather than for a significant expansion strategy.

Traditionally, GEO satellites have been large, complex and expensive to build and launch. However, the industry is witnessing a paradigm shift toward smaller GEO satellites, which offer numerous advantages over their larger counterparts. These benefits include reduced manufacturing and launch costs, shorter development cycles and increased flexibility in deployment and operation.

Furthermore, the reduced costs and increased flexibility of small GEO satellites support the growth of satellite constellations and hybrid networks. These networks, combining GEO satellites with NGSO satellites, can deliver enhanced coverage, capacity and resilience. This hybrid approach is particularly valuable for applications like global broadband internet, where consistent and reliable coverage is essential.

One good example is Swissto12, a 3D-printed subsystem RF specialist that entered the satellite integrator scene with its HummingSat, a 1-ton class satellite. Swissto12 is leveraging cutting-edge manufacturing techniques, like 3D printing, to produce satellite components. This method reduces production times and costs, while also allowing for more complex and lightweight structures that traditional manufacturing methods cannot achieve. The company advertises better economics for its customers’ business plans which wouldn’t close otherwise with a larger form factor.

On top of form factor diversity, business model innovation is at full speed, too. Astranis operates under a vertically integrated model and leases its 500 kg micro-GEOs, built and operated in-house. Such an offer has secured momentum from customers who do not want to put upfront the CAPEX and operate satellites on their own.

Can Software-Defined Satellites’ Flexibility Offset Higher Costs?

One of the most significant shifts in satellite technology is the adoption of software-defined payloads. Traditional satellites often had fixed functionalities, limiting their adaptability. However, with software-defined payloads, operators can reconfigure satellite missions on the fly to meet changing requirements.

Airbus, Thales, Maxar and Boeing have been developing satellites with advanced software capabilities, allowing for dynamic reprogramming to optimize performance and extend the satellite’s operational life. This flexibility is particularly valuable in an environment where market demands and technological landscapes are rapidly changing. Nevertheless, as any new development, the rollout of such payloads has proved to be quite complicated and translated into cost increases and delays. The higher-than-expected cost of such new satellites has proven to be challenging for some operators beyond early adopters, but market adoption may grow after maiden launches.

Sustainable Practices and Materials

Sustainability is becoming a priority in satellite manufacturing. With growing concerns about space debris and the environmental impact of satellite launches, manufacturers are adopting greener practices and materials. The use of lightweight, durable materials, like carbon fiber composites, reduces the overall weight and launch costs. Moreover, initiatives like the development of satellite end-of-life disposal mechanisms and the design of satellites to burn up upon reentry are helping mitigate space debris issues.

High Expectations for Very Low Earth Orbit

VLEO’s proximity to Earth offers unique advantages in terms of reduced latency, higher resolution imaging and lower power requirements for communication. Operating in VLEO is not without its challenges. Satellites face increased atmospheric drag, radiation exposure and thermal stresses. However, manufacturers stated these products have a role in the market.

An image of Redwire’s Very Low Earth Orbit platform, Phantom, developed through the European Space Agency’s Skimsat VLEO mission. (Source: Redwire)

An image of Redwire’s Very Low Earth Orbit platform, Phantom, developed through the European Space Agency’s Skimsat VLEO mission. (Source: Redwire)

Redwire, a prominent player in the space industry, has unveiled the Skimsat satellite bus, designed specifically for VLEO operations. Skimsat is engineered to withstand the harsher atmospheric conditions and increased drag experienced at these lower altitudes. Key features of Skimsat include advanced materials for thermal protection, enhanced propulsion systems for drag compensation and innovative power management to extend operational lifespan.

Capitalizing on Low-Cost Launches: The Starship Opportunity

Super heavy launchers, like SpaceX’s Starship, are paving the way for ambitious future space missions with a focus on delivering crew landers to the Moon as part of NASA’s Artemis program. K2 Space aside, most satellite manufacturers are taking a cautious approach toward this new launch supply. One key advantage of super heavy launchers, like Starship, is their ability to accommodate larger payloads in a single launch. This allows satellite manufacturers to reconsider the dimensions and configurations of their satellites, enabling them to take full advantage of the increased payload capacity. This, in turn, can lead to cost efficiencies and enhanced capabilities for satellite missions.

Commercial space station projects, like Starlab or Gravitics, are early customers of these launchers by leveraging the 9-meter diameter payload fairing and unmatched volume to provide vast habitats to their crews in one single launch. While Starship has yet to launch successfully, adapting satellite designs to leverage the capabilities of the super heavy launcher involves rethinking traditional size constraints. Super heavy launchers may trigger design changes in satellite design through more powerful satellites (larger optics, antennas, solar panels and more fuel, enabling longer lifespans and improving the economics of satellite operators) or simpler, less costly and complex design and development.

Conclusion

The satellite manufacturing industry is in the midst of a significant transformation, driven by the need for greater efficiency, flexibility and sustainability. By embracing small satellite technology, advanced propulsion systems, modular designs, AI, enhanced communication technologies and sustainable practices, manufacturers are not only surviving but thriving in a competitive landscape. These innovations promise to expand the possibilities of what satellites can achieve, from improving global communications to enhancing our understanding of the planet. By staying ahead of technological trends and understanding market demands for new products, they aim to win new business and also shape the future of satellite infrastructure.

About the Author

Maxime Puteaux leads Novaspace’s space industry consulting practice (merger of Euroconsult and Space Tech) covering topics related to upstream activities in the satellite value chain, such as access to space, manufacturing and in-orbit operations. Maxime authored several flagship market intelligence reports. He joined the company in 2012.

Explore More:

Podcast: The Evolving Maritime Market, Offices at Sea and the Impact of Starlink

Podcast: Software, Satellites and a More Dynamic World

Big Interest in Small GEO: Why Satellite Operators Are Intrigued

Satellite Manufacturers Adapt Supply Chains Amid Demand for Mass Production