PARIS - In an increasingly complex global security environment, space has emerged as a critical domain for military operations. The role of space in defense and security has expanded beyond traditional uses to include a wide array of strategic capabilities. These capabilities are essential for national security, providing countries with intelligence, surveillance, reconnaissance, secure communications, and positioning, navigation, and timing (PNT) services that are indispensable in modern warfare. This article explores the key trends, investments, and challenges in the space security and defense sector as nations adapt to the growing demands of space as a contested and militarized domain.

Space as a Strategic Military Domain

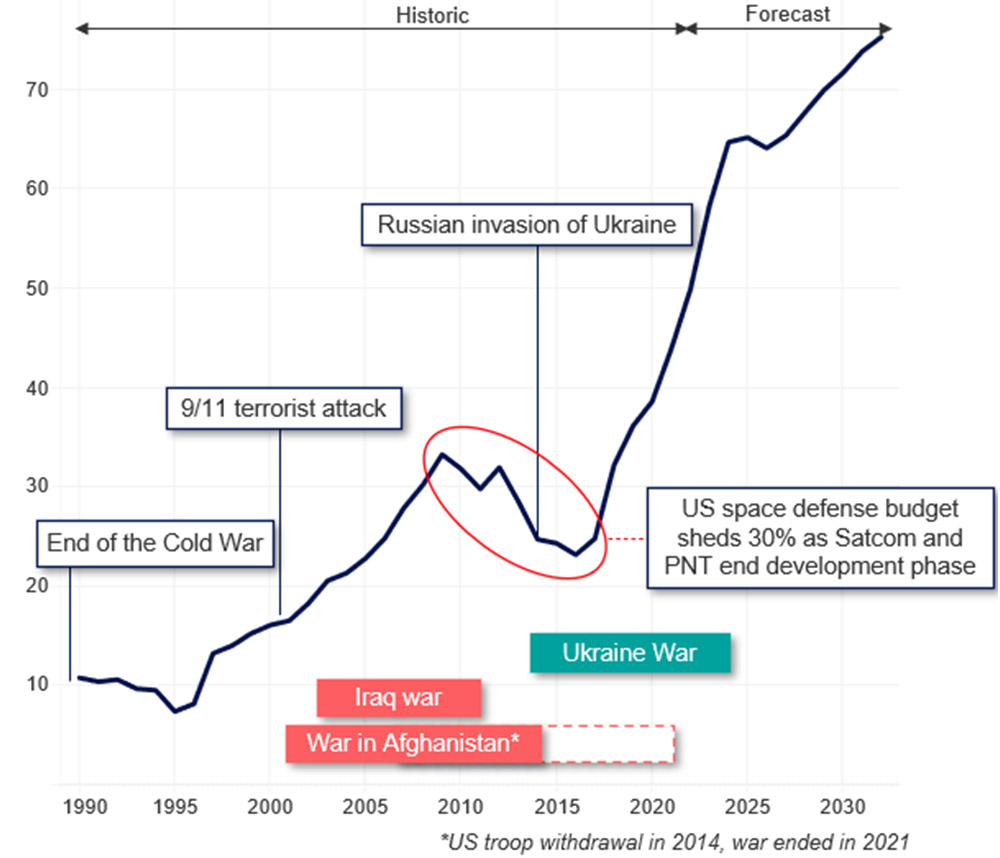

Space has long been recognized as a strategic asset in military operations. The earliest widespread use of space-based assets occurred during the 1991 Gulf War, where the U.S. military effectively integrated GPS for precision navigation and secure satellite communications for command and control operations. Since then, space capabilities have become integral to national defense strategies globally. Today, space is not just a support domain but a battleground where countries are developing capabilities to protect their assets and deny adversaries the same.

Figure 1: Global government expenditures on space defense and security, in US$ billions (Source: Novaspace)

Figure 1: Global government expenditures on space defense and security, in US$ billions (Source: Novaspace)

Global Expenditures in Space Defense

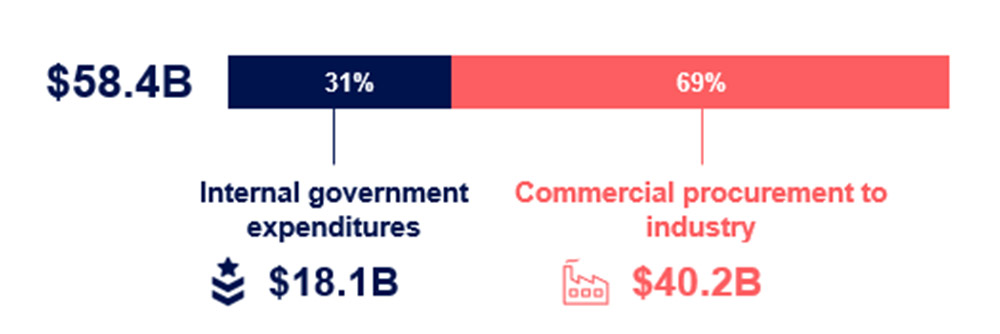

In 2023, global government expenditures on space defense and security reached an unprecedented $58.4 billion, driven by the need to enhance national security in an increasingly contested space environment. This represents a significant increase from previous years, nearly doubling from $32.2 billion in 2018, with a compound annual growth rate (CAGR) of 12.6% over the past five years. The rise in spending is a direct response to escalating geopolitical tensions and the recognition of space as a critical warfighting domain.

Of the total $58.4 billion in government spending, a significant portion is contracted out to the commercial sector. In 2023, over two-thirds of this amount, approximately $40.2 billion, represents the revenues generated by the industry for providing space defense and security capabilities to governments. These industry revenues are derived from four primary segments of the value chain: the manufacture and launch of defense satellites, the provision of user terminals (especially for SATCOM and PNT), the commercial operation of satellite systems, and the supply of commercial products, data, and services to defense organizations.

Figure 2: Split of government expenditures and industry revenues in 2023 (Source: Novaspace)

Figure 2: Split of government expenditures and industry revenues in 2023 (Source: Novaspace)

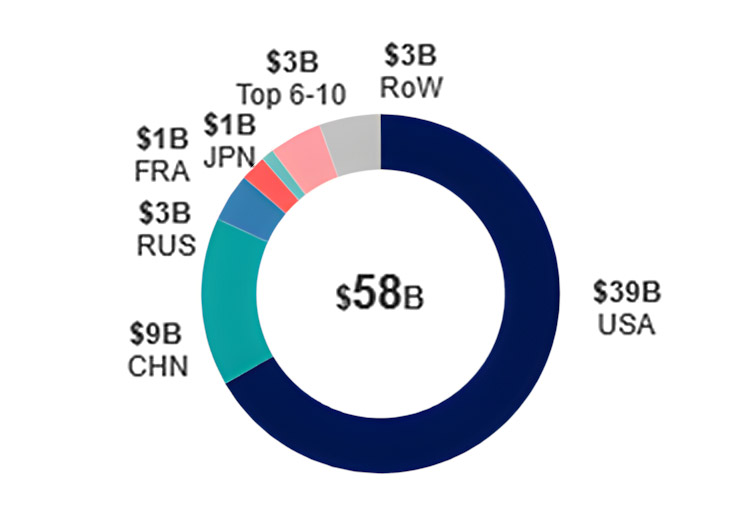

The United States leads these investments with $38.9 billion, followed by China at $8.8 billion, Russia at $2.6 billion, France at $1.3 billion, and Japan at $716 million. These five countries alone account for about 90% of the global spending, reflecting their strategic focus on maintaining and expanding their space capabilities.

Figure 3: Space defense & security expenditures in 2023 by country (Source: Novaspace)

Figure 3: Space defense & security expenditures in 2023 by country (Source: Novaspace)

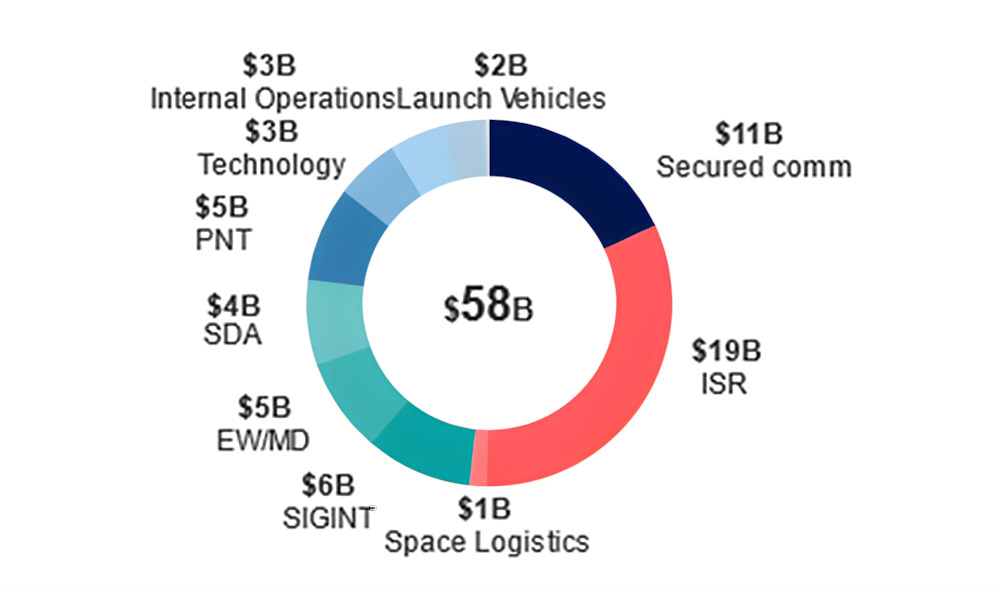

Expenditures are distributed across several key capability domains, with Intelligence, Surveillance, and Reconnaissance (ISR) accounting for the largest share at 32% or $18.8 billion. Secured Satellite Communications follow with 18% ($10.6 billion), highlighting the critical role of communications in military operations. Signal Intelligence (SIGINT), Positioning, Navigation, and Timing (PNT), and Space Domain Awareness (SDA) are other significant areas of investment.

Figure 4: Space defense & secuity expenditures in 2023 by capability domain (Source: Novaspace)

Figure 4: Space defense & secuity expenditures in 2023 by capability domain (Source: Novaspace)

The Shift Toward Resilience and Proliferation

The growing dependence on space assets for military operations has made these systems targets for adversaries. To mitigate the risks associated with potential attacks, there is a shift towards developing resilient and proliferated architectures. The U.S. Space Force, for instance, is investing heavily in proliferated low Earth orbit (LEO) constellations, which offer redundancy and reduce the risk of a single point of failure.

Countries are also focusing on improving their Space Domain Awareness (SDA) capabilities to better monitor and protect their space assets. This includes tracking an increasing number of Resident Space Objects (RSOs), including both active satellites and space debris. SDA capabilities are essential for identifying potential threats and ensuring the safety and operational effectiveness of space-based systems.

Emerging Threats and Counterspace Capabilities

The militarization of space has led to the development of counterspace capabilities by leading space powers. The U.S., China, and Russia are at the forefront of these efforts, developing technologies that can degrade, disrupt, or destroy adversary space assets. These capabilities include kinetic physical attacks, such as anti-satellite (ASAT) weapons, and non-kinetic methods, such as jamming, spoofing, and cyberattacks.

One of the most significant challenges in this domain is the proliferation of these technologies, making them increasingly accessible to a broader range of actors, including non-state entities. This proliferation increases the risks of conflict in space, as more players acquire the means to interfere with or damage critical space infrastructure.

The Role of Commercial Entities

The growing demand for space-based services has also opened up opportunities for commercial entities. Governments are increasingly relying on commercial satellite providers to augment their proprietary systems, particularly in ISR and secured communications. Companies like SpaceX, through its Starshield program, are developing capabilities tailored for government use, including the deployment of ISR payloads in LEO.

This trend towards commercial involvement is driven by the need for rapid innovation and deployment, areas where commercial companies often outpace government efforts. However, this also raises concerns about the security of commercially operated systems and the potential for these assets to become targets in a conflict.

Where Do We Go from There?

Defense actors must take strategic steps to navigate the evolving space security landscape effectively. The first priority should be enhancing resilience in space architectures. The shift toward proliferated LEO constellations is a critical response to vulnerabilities of traditional, centralized space systems. Defense actors should accelerate investments in these resilient architectures, ensuring that their space assets can withstand potential attacks, including both kinetic and non-kinetic threats.

Next, there should be a concentrated effort on advancing SDA. The ability to monitor, track and respond to threats in space is increasingly vital as the number of RSOs continues to grow. Defense actors must invest in technologies and capabilities that enhance their situational awareness in space, enabling them to detect and mitigate threats proactively.

In the near to medium term, defense actors should also anticipate the continued proliferation of counterspace technologies. This means preparing for a future where not just state actors, but potentially non-state entities, possess the capabilities to disrupt or destroy critical space infrastructure. Developing countermeasures, both defensive and offensive, will be essential to maintaining strategic superiority.

Furthermore, defense actors should seek to establish robust partnerships with commercial providers, leveraging their innovation and agility while also addressing the security and interoperability concerns associated with commercially operated systems. This collaboration will be crucial in ensuing that commercial capabilities complement national defense strategies without compromising security.

Conclusion

As space continues to evolve into a contested and militarized domain, nations are making substantial investments in their space defense and security capabilities. The increasing reliance on space-based assets for military operations underscores the need for resilient and secure systems. At the same time, the development of counterspace capabilities and the involvement of commercial entities introduce new challenges and complexities. Moving forward, the ability of nations to protect their space assets and maintain operational superiority in space will be crucial in shaping the future of global security.

In this rapidly changing environment, the strategic importance of space will only grow, making it imperative for governments and industry players alike to stay ahead of emerging threats and continue to innovate in this critical domain. For a more in-depth analysis and comprehensive data on these trends, refer to the Space Defense and Security report issued by Novaspace (formerly Euroconsult).

About the Author:

Candice Massucci-Templier is a Senior Consultant at Novaspace, based in Paris. She specializes in European space policies and government strategies, with a focus on analyzing space programs and policies.