Originally published by Analysys Mason on February 12, 2025. Read the original article here.

“Most European countries are moving towards a market structure dominated by three major MNOs.”

Most European countries are moving towards having three major MNOs.

The share of Europeans living in a country with no more than three MNOs is expected to grow by 10 percentage points to 56% from 2015 to 2025, as a result of recent market consolidations (recent examples include the MÁSMÓVIL–Orange and Vodafone–Three mergers in Spain and the UK, respectively).

Only a few recent fourth market entrants have gained a large market share in connections (as the data included in Analysys Mason’s DataHub shows) and have significantly influenced the markets they entered. Iliad, in Italy, is one example of this – it entered the market in 2019 and has since gained a 16% market share in mobile connections in 6 years (despite reporting losses for its Italian operations).1 Digi is hoping to replicate Iliad’s success in Belgium, Portugal and Spain.

However, most fourth market entrants have struggled to gain market share. This trend appears to be global, as international comparisons indicate that it is challenging for fourth market entrants to succeed in the markets they enter.

MVNOs across Europe have mostly failed to increase their market share. Their share of mobile connections grew marginally, to around 10%, in the period from 2015 to 2024.2

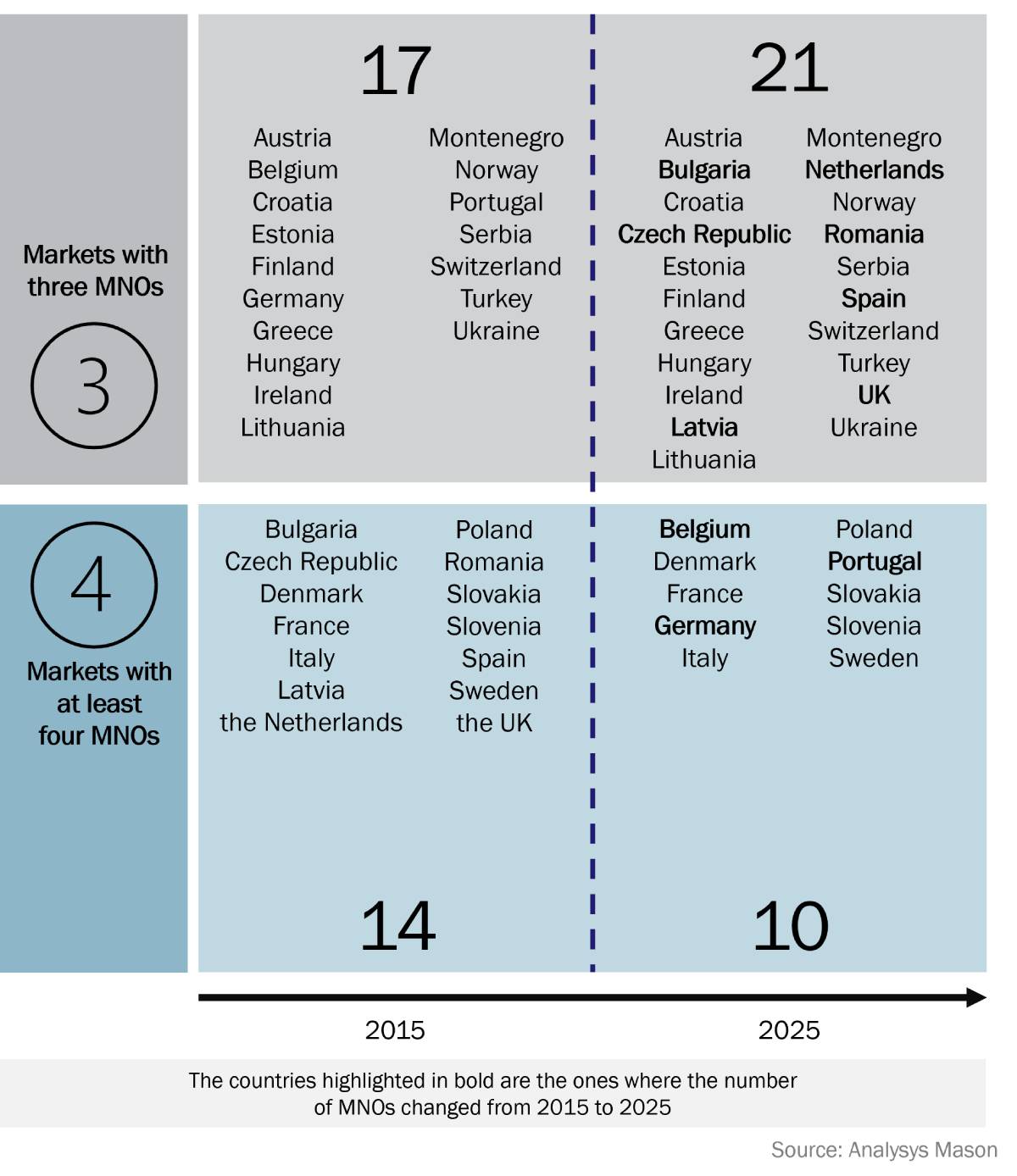

The number of MNOs is falling in many European countries

The number of European countries with three MNOs is expected to increase from 17 in 2015 to 21 in 2025 (see Figure 1).

Several mergers were completed (or received regulatory approval) in the last 10 years. These deals fall mainly under two categories.

- A merger between two relatively large MNOs that were finding it difficult to compete with the market leader (such as the MÁSMÓVIL–Orange and Vodafone–Three mergers in Spain and the UK, respectively).

- A relatively large MNO purchases a small/regional MNO, often because the latter was in a difficult financial situation (such as the (planned) acquisition of Nordic Telecom by O2 in the Czech Republic).

The European Commission (EC) refused a few deals that would have reduced the number of MNOs from four to three in some countries (or allowed the transaction with strict conditions).3

- Italy remained a market with four MNOs even after the EC allowed the merger between Tre and Wind, on the condition that the two MNOs sell their assets to the new market entrant (Iliad).4

- In Spain, the EC approved the joint venture between MÁSMÓVIL and Orange, provided they made a series of concessions to benefit the MVNO Digi.5

By 2025, the number of MNOs will have increased from three to four in just three countries: Belgium, Germany and Portugal.

Figure 1: Number of MNOs by country, Europe, 2015 and 2025

Most fourth market entrants have struggled to succeed beyond Europe

Several new fourth mobile market entrants have launched in the past 10 years, worldwide. They have generally struggled to either gain scale or be profitable (or both), with a few exceptions. The following are examples of new, fourth market entrants worldwide.

- In China, CBN only had a 2% market share in mobile connections in 2Q 2024, 2 years after its launch.

- In Japan, (former MVNO) Rakuten launched its mobile network in 2020. It had a 4.2% market share in connections in 2Q 2024 (it lost almost 500 000 customers in 2022 because it stopped offering its initial promotional offering that included up to 1GB per month at JPN0).

- In South Korea, Stage X failed to raise enough capital to deploy its 5G network. The government decided to withdraw its 5G licence in July 2024.

- In the USA, DISH is deploying a 5G network (a cloud-native, Open RAN 5G network) at a slower rate than planned. In September 2024, the regulator (the Federal Communications Commission) accepted DISH’s request to extend (by at least 12 months) some of its 5G roll-out deadlines.6

In Europe, the MVNO 1und1 shares the same difficulties with the fourth market entrants mentioned above.

Indeed, in Germany, 1und1 faces several challenges to deploy its 5G network and migrate customers from Telefónica’s network to its network (it migrated around 5% of its customer base (700 000 customers) in 1Q 2024). The network outage that occurred in May 2024 significantly slowed the migration process during the second half of 2024.

Iliad (in Italy) is the main exception to fourth market entrants struggling to gain market share. Iliad reached a 16% market share in mobile connections 6 years after entering the market.7 However, it continues to post losses (it needs a long-term plan to generate profits).8

In the future, most Europeans will likely, de facto, choose from three major mobile network operators

The share of Europeans that live in a country with fewer than four MNOs is expected to grow from 46% in 2015 to 56% by the end of 2025.

MVNOs have struggled to gain market share beyond budget-conscious customers and may struggle to notably grow their user base. Their share of mobile connections grew by just one percentage point (to 10%) from 2015 to 2024.

If we consider how many fourth market entrants struggled to gain scale worldwide in recent years, it seems likely that more and more customers in Europe will have three MNOs to choose from in the future.

1 For more information, see Analysys Mason’s European Country Reports and European Quarterly Metrics research modules.

2 For more information, see Analysys Mason’s DataHub. It includes data for data for MNOs and MVNOs in around 80 countries worldwide.

3 In Denmark, the commission raised concerns about the proposed merger between Telia and Telenor in 2015; in the UK, it opposed the merger between O2 and Three in 2016 (this decision was later overturned and discussions continue whether the EC made the right choice to block the merger).

4 European Commission (31 August 2018), Mergers: Commission clears acquisition of sole control of Wind Tre by Hutchison, subject to conditions.

5 MÁSMÓVIL transferred 60MHz of spectrum (in the 1800MHz, 2100MHz and 3500MHz frequency bands) to Digi. Digi obtained the right to sign a national mobile roaming agreement with MÁSMÓVIL and Orange (Digi has the right to exercise this option). For more information, European Commission (20 February 2024), Commission approves joint venture between Orange and MásMóvil in Spain, subject to conditions.

6 Federal Communication Commission (18 September 2024), 2024-09-18 Letter from EchoStar Corporation.

7 For more information about Iliad Group’s strategy, please see Analysys Mason’s Iliad’s central telecoms strategy is similar to that of most operators, but the details have lessons for others.

8 Iliad posted a loss of EUR168 million in the 9-month period to 3Q 2024 (it was EUR257 million in the 9-month period to 3Q 2023).

Originally published by Analysys Mason on February 12, 2025. Read the original article here.